{kind=link}

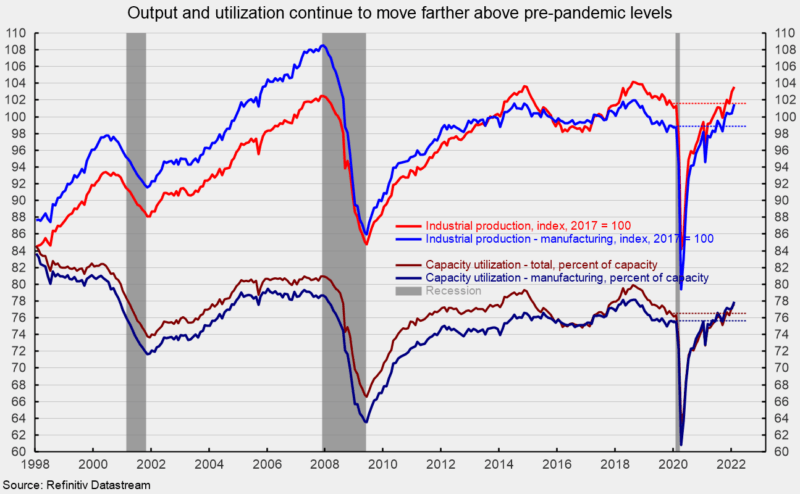

Industrial production gained 0.5 percent in February despite a reversal of the weather-related surge in utility output in January. The gain pushes total industrial output to its highest level since December 2018, and clearly above the December 2019 level prior to the pandemic (see first chart). Over the past year, total industrial output is up 7.5 percent.

Total industrial capacity utilization increased 0.3 points to 77.6 percent from 76.3 percent in January, the highest since March 2019 (see first chart). However, total capacity utilization remains well below the long-term (1972 through 2021) average of 79.5 percent.

Manufacturing output – about 74 percent of total output – posted a more robust 1.2 percent increase for the month (see first chart). Manufacturing output is at its highest level since September 2018 and is 2.9 percent above its January 2019 pre-pandemic level (see first chart). From a year ago, manufacturing output is up 7.4 percent.

Manufacturing utilization increased 0.9 points to 78.0 percent, well above the December 2019 level of 75.6 percent and the highest level since September 2018, but just slightly below its long-term average of 78.1 percent. However, it remains well below the 1994-95 high of 84.7 percent (see first chart).

Mining output accounts for about 14 percent of total industrial output and posted a modest 0.1 percent increase last month (see top of second chart). Over the last 12 months, mining output is up 17.3 percent. Utility output, which is typically related to weather patterns and is about 12 percent of total industrial output, sank 2.7 percent, partially reversing the January surge of 10.4 percent (see top of second chart) with natural gas off 12.1 percent and electric down 0.9 percent. From a year ago, utility output is off 1.2 percent.

Among the key segments of industrial output, energy production (about 27 percent of total output) fell 1.0 percent for the month (see bottom of second chart) with declines across four of the five components. Total energy production is up 9.3 percent from a year ago and is back slightly below the December 2019 level (see third chart).

Motor-vehicle and parts production (slightly under 5 percent of total output), one of the hardest-hit industries during the lockdowns and post-lockdown recovery, continues to struggle with a semiconductor chip shortage. Motor-vehicle and parts production fell 3.5 percent in February following a 0.3 percent drop in January and a 1.1 percent fall in December (see bottom of second chart). From a year ago, vehicle and parts production is unchanged, but compared to December 2019, output is off 7.4 percent (see third chart).

Total vehicle assemblies fell to 8.43 million at a seasonally-adjusted annual rate. That consists of 8.15 million light vehicles and 0.28 million heavy trucks. Within light vehicles, light trucks were 6.66 million while cars were 1.49 million. Light-vehicle assemblies are still more than 20 percent below December 2019 levels (see third chart).

The selected high-tech industries index jumped 1.8 percent in February (see bottom of second chart), and is up 7.8 percent versus a year ago, and about 19 percent above December 2019 (see third chart). High-tech industries account for just 1.9 percent of total industrial output.

All other industries combined (total excluding energy, high-tech, and motor vehicles; about 67 percent of total industrial output) rose a strong 1.4 percent in February (see bottom of second chart). This important category is 7.3 percent above February 2021 and 3.1 percent above December 2019 (see third chart). Industrial output posted a gain in February despite a significant drop in utility output. Industries outside of energy and motor vehicles generally posted a strong gain for the month. However, ongoing disruptions to labor supply, rising costs and shortages of materials, and logistics and transportation bottlenecks continue to be challenges for the industrial sector. While cresting numbers of new Covid cases in late January and early February had the potential to support businesses’ efforts to improve supply chains and expand production, geopolitical turmoil surrounding the Russian invasion of Ukraine has had a dramatic impact on capital and commodity markets, launching a new wave of potential disruptions to businesses.