{kind=link}

Credit markets are becoming increasingly vulnerable to fallout from the emerging trade war. While the media will continue to focus on headline tariff announcements and retaliatory measures, structural risks are emerging. Trade frictions are being transmitted into funding markets, onto corporate balance sheets, and ultimately into broader economic activity.

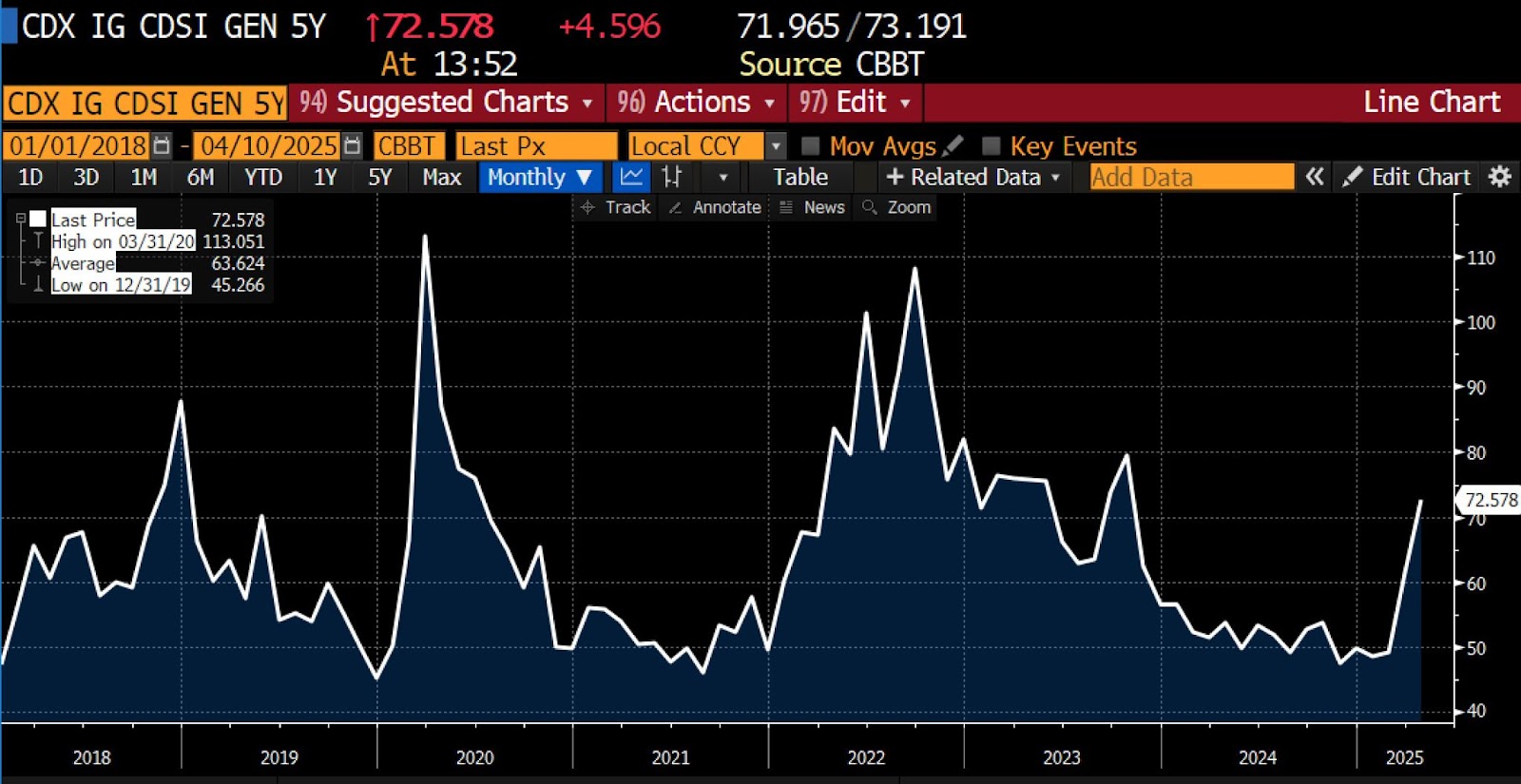

Tariffs risk triggering a credit event that could spill into broader financial markets and catalyze a recession. Credit quality is like a credit score for companies, measuring financial solvency, the likelihood that a company (or government) will default on its loans. Credit spreads — the premium that investors demand to hold risky corporate bonds over nominally risk-free Treasury securities — have already begun to widen. That widening reflects rising concern about credit risk, as investors require higher compensation to hold debt issued by companies rather than the US government.

Corporate earnings, particularly for export-oriented and cyclical sectors, are sensitive to trade volumes. As trade volumes contract, revenues follow. That same pressure then reduces profit margins, downgrades credit quality, and increases the risk of default.

Markit CDX North America Investment Grade Index, 5 year (2018 – present)

The historical relationship between global trade and high-yield credit spreads is well documented. Economies such as South Korea and Taiwan, which are deeply embedded in global manufacturing supply chains, tend to serve as proxies for global trade health. Their export performance tends to move in tight correlation with US high-yield spreads. While spreads have not yet reached the extremes observed during the 2020 liquidity crisis or the 2022 tightening cycle, the trajectory is clear and disconcerting.

The core concern is a pernicious cascade: deteriorating trade activity feeding into weaker corporate cash flows; those widen spreads, raise borrowing costs, and suppress investment. Tighter financial conditions then further dampen trade and output. It is a dynamic which is more likely to become self-reinforcing than not. And once credit spreads surpass a certain threshold, the cost of capital rises to levels that materially affect hiring decisions, capital expenditures, and the management of working capital. Planned expansions, acquisitions, and mergers will be cancelled. For highly leveraged firms, particularly in the high-yield (“junk bond”) space, refinancing becomes punitive if not impossible. Defaults rise, liquidity tightens, and layoffs follow. This is how downturns begin — not with a dramatic event, but with a slow erosion of credit quality and confidence.

Despite an equity market correction of over 10 percent from February 2025 highs, valuations remain elevated relative to where they tend to settle during recessions. Historical analogs suggest that if a recession materializes, a total drawdown in equities of 30 percent is plausible. Yield curves have been inverted for a long enough period that their signal has reduced significance, at least in the present cycle, but other recession indicators, including the Sahm Rule, have been triggered.

Markit CDX North America High Yield Index, 5 year (2018 – present)

Compounding the risk is a growing reassessment of US Treasurys as a safe haven. To be sure: this reevaluation is an objective of the Trump administration as part of its larger “Mar-a-Largo Accord” plans. Despite a clear risk-off stance across asset classes (note Bitcoin’s decline, even as gold rises) Treasury yields have moved higher, suggesting that concerns over fiscal sustainability and geopolitical risk are outweighing traditional flight-to-safety dynamics. As a result, the usual stabilizing function of the Treasury market has become less reliable.

This is a particularly problematic development for credit markets. A functioning Treasury market is essential for collateral chains, repo markets, and swap pricing. As volatility in government bonds rises, so too does the cost of financing credit exposure.

A sharp selloff in junk bonds following President Trump’s tariff escalation has doubled refinancing costs for high-yield borrowers this year, raising fears that the market could become inaccessible for weaker issuers. With average yields on US and European junk indexes surging to multi-year highs, deal cancellations, fund outflows, and widening credit spreads suggest growing liquidity stress that could dampen investment and trigger a self-reinforcing default cycle if access to funding remains constrained.

A further complication comes from the ballooning use of basis trades — leveraged strategies in which hedge funds go long on cash bonds and short bond futures, typically funded through repo markets. These trades are used to capture tiny arbitrage spreads, and now provide a critical plumbing component of fixed income markets. As credit weakens and volatility rises, margin calls and funding costs escalate. Bond funds, facing redemption pressure, may be forced to liquidate holdings, triggering a feedback loop of selling and deleveraging. The unwinding of basis trades was a key contributor to the March 2020 Treasury market dysfunction. The risk is greater now, given the larger scale of the trades and tighter dealer balance sheets.

Chicago Board Options Exchange Volatility Index and Gold USD (2021 – present)

In a severe scenario, the Federal Reserve could be compelled to intervene directly—perhaps via a dedicated facility to support Treasury funding or address basis trade dislocation. But such action would likely come only after substantial market dislocation and much of the damage would be done by the time such a facility was made available.

Tariffs are not simply a geopolitical tactic—they are a blunt instrument with the potential to generate far-reaching market implications. While outcomes remain uncertain, the risk of a cascading disruption is evident. Elevated tariffs suppress global trade volumes, which in turn weigh on corporate earnings. Weaker earnings undermine credit quality, increasing default risk. And in an interconnected global economy, defaults in one sector can quickly transmit across others through financial and supply-chain linkages.

A not quite old, but older, trader’s instinct is that credit markets are becoming a primary transmission vector by which tariff stress infiltrates the wider economy. Once spreads widen sufficiently and liquidity tightens, recession risk rises sharply. When credit breaks, every other corner of the economy inevitably follows.