{kind=link}

The selling rate of existing homes decreased 2.4 percent in April, to a 5.61 million seasonally adjusted annual rate. The selling rate is down 5.9 percent from a year ago.

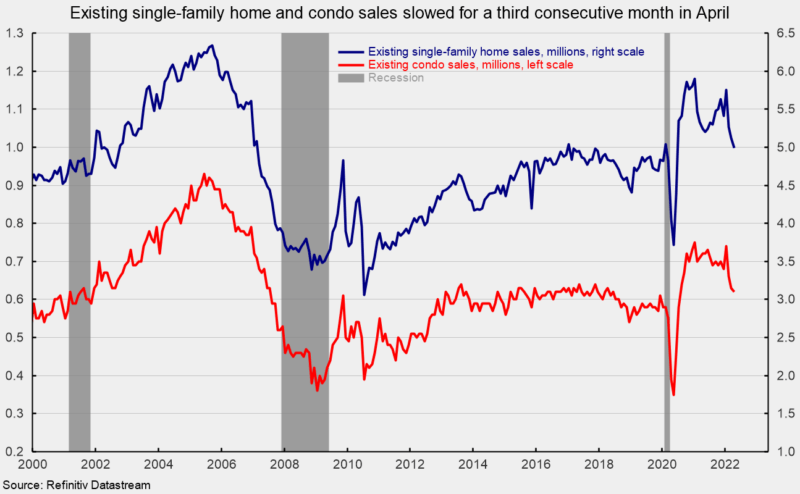

The selling rate in the market for existing single-family homes, which account for about 89 percent of total existing-home sales, fell 2.5 percent in April, coming in at a 4.99 million seasonally adjusted annual rate, the first month below 5 million since June 2020 (see first chart). From a year ago, the selling rate is down 4.8 percent.

The single-family segment saw slowing sales in two of the four regions. Sales slowed 6.5 percent in the West and 5.6 percent in the South, the largest region by volume, while sales accelerated 3.7 percent in the Northeast, the smallest region by volume, and accelerated 4.2 in the Midwest. Measured from a year ago, sales were slower in all four regions (-11.1 percent in the Northeast, -8.3 percent in the West,-3.5 percent in the South, and -0.8 percent in the Midwest).

Condo and co-op sales slowed by 1.6 percent for the month, leaving sales at a 620,000 annual rate for the month, their slowest pace since July 2020, versus 630,000 in March (see first chart). From a year ago, condo and co-op sales were 13.9 percent slower. Condo and co-op sales were slower in two regions in April, -11.1 percent in the Midwest and -8.3 percent in the Northeast, but unchanged in the West and 3.6 percent faster in the South. From a year ago, sales were slower in all four regions (-19.4 percent in the South, -11.1 percent in the Midwest, -8.3 percent in the Northeast, and -6.7 percent in the West).

Total inventory of existing homes for sale rose in April, increasing by 10.8 percent to 1.03 million (the first result above one million since November) leaving the months’ supply (inventory times 12 divided by the annual selling rate) up 0.3 month at 2.2, the highest since October, but still extremely low by historical comparison.

For the single-family segment, inventory was up 12.3 percent for the month at 910,000 (see second chart) but is 7.1 percent below the April 2021 level. The months’ supply was 2.2, up from 1.9 in the prior month (see third chart).

The condo and co-op inventory was unchanged at 118,000 (see second chart), leaving the months’ supply at 2.3, up from 2.2 in March. Months’ supply is 17.9 percent below April 2021 (see third chart).

The median sale price in April of an existing home was $391,200, 14.8 percent above the year ago price. For single-family existing home sales in April, the price was $397,600, also a 14.8 percent rise over the past year and a record high (see fourth chart). The median price for a condo/co-op was $340,000, 13.1 percent above April 2021 and a record high (see the fourth chart).

Housing is likely to be volatile over the coming months as fundamentals adjust to changing market conditions. Increased opportunities for employees to work remotely are likely to impact demand while supply chain issues and labor difficulties impact supply. Furthermore, record-high prices and the recent surge in mortgage rates will likely push some buyers out of the market.