{kind=link}

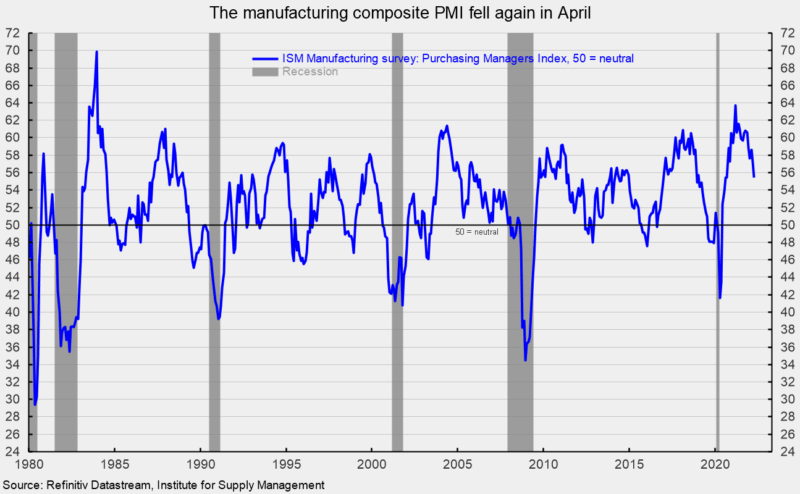

The Institute for Supply Management’s Manufacturing Purchasing Managers’ Index fell to 55.4 in April, off 1.7 points from 57.1 percent in March (50 is neutral). April is the 23rd consecutive reading above the neutral threshold but the level continues to trend lower from the March 2021 peak (see first chart). The survey results indicate that the manufacturing sector continues to expand but price pressures remained significant, labor shortages from quits and retirements continued to be a headwind, and supply-chain disruptions lingered. However, survey respondents remained optimistic about future demand.

The Production Index registered a 53.6 percent result in April, a drop of 0.3 points from March. The index has been above 50 for 23 months but is at its lowest level since the plunge in early 2020 (see top of second chart).

The Employment Index posted a sharp decline in April, coming in just barely above neutral at 50.9 percent, suggesting little change to employment levels (see top of second chart). The Bureau of Labor Statistics’ Employment Situation report for April is due out on Friday, May 6, and expectations are for a gain of 380,000 nonfarm payroll jobs including the addition of 35,000 jobs in manufacturing.

The new orders index lost 0.3 points to 53.5 percent in April. It has been above 50 for 23 consecutive months but is at the lowest level since the post-lockdown plunge (see bottom of second chart). The new export orders index, a separate measure from new orders, fell to 52.7 versus 53.2 in March. The new export orders index has been above 50 for 22 consecutive months.

The Backlog-of-Orders Index came in at 56.0 versus 60.0 in March, a 4-point decline (see bottom of second chart). This measure has pulled back from the record-high 70.6 result in May 2021 but has been above 50 for 22 consecutive months. The index suggests manufacturers’ backlogs continue to rise but that the pace decelerated in April.

Customer inventories in April are still considered too low, with the index coming in at 37.1, up 3.0 points from March (index results below 50 indicate customers’ inventories are too low). The index has been below 50 for 67 consecutive months. Insufficient inventory is a positive sign for future production.

The index for prices for input materials eased slightly in April, falling 2.5 points to 84.6 percent versus 87.1 percent in March (see third chart). The index has climbed back towards the recent peak of 92.1 in June 2021 and suggests price pressures remain intense. Meanwhile, the supplier deliveries index registered a 67.2 result in April, up 1.8 points from the March result. The rise suggests deliveries slowed again in April and that the pace accelerated for the second time in the last three months (see third chart).

Demand for the manufacturing sector remained strong in April and survey respondents remained optimistic that the strong demand will continue. However, labor difficulties, materials shortages, and logistical problems continue to hamper the ability to meet that demand. Furthermore, the Russian war against Ukraine and lockdowns in China in response to surging COVID-19 cases are sparking new sources of disruptions to global supply chains.