{kind=link}

Summary

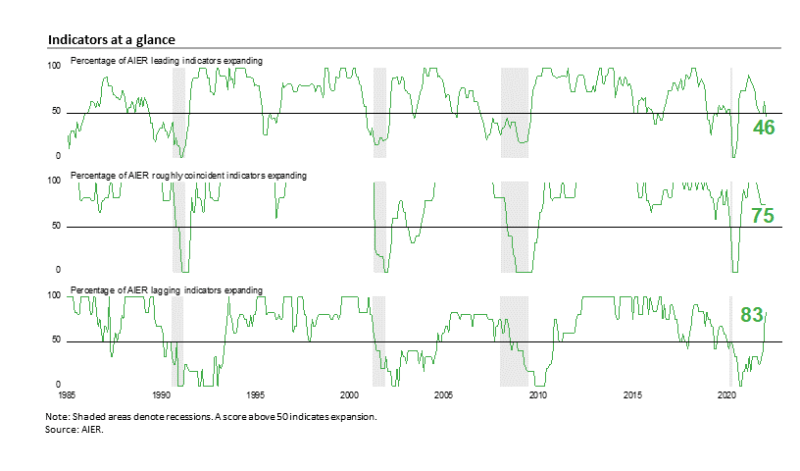

AIER’s Leading Indicators Index posted a surprising 17-point drop in February, more than erasing the solid 13-point gain in January. The Leading Indicators Index dropped to 46 from 63 in January and follows three consecutive months at the neutral 50 mark from October through December. The drop matches a similar decline in August 2021, tying for the largest one-month decrease since May 2020. The Roughly Coincident Indicators Index was unchanged again in February, holding at 75 for a fourth consecutive month, while the Lagging Indicators Index posted an 8-point gain and is at its highest level since December 2018 (see chart).

Just one month after all three AIER business cycle indicators turned positive, suggesting an improving outlook, multiple yellow flags have emerged. While the cresting of new Covid cases was a clear positive development that supported efforts by businesses to refocus on boosting output and easing supply chain issues, geopolitical events have sent shockwaves through financial markets and the global economy. Increased volatility should be expected to continue in capital and commodity markets and begin to show through in economic statistics over coming months. Both are likely to cause volatility for the AIER business cycle indicators as well. Extreme caution is warranted.

AIER Leading Indicators Index Drops Below Neutral in February

The AIER Leading Indicators index posted a surprise drop in February, falling 17 points and more than offsetting the 13-point gain in January. The February level is the first reading below neutral since August 2020 in the wake of government lockdowns that sent the U.S. economy to the worst recession in history. The February result follows a 63 result in January and three consecutive months at the neutral 50 level for October through December.

Three leading indicators changed signal in February, each for the worse: the manufacturing and trade sales-to-inventory indicator weakened from a favorable trend to a neutral trend as did the real new orders for core capital goods indicator. The debit balances in margin accounts indicator weakened sharply, dropping from a positive trend to a negative trend. Among the 12 leading indicators, just four were in a positive trend in February while five were trending lower and three were trending flat or neutral. Adding to the concern is the strong likelihood that the real stock price indicator will flip to a negative trend from its current positive trend given the sharp decline in nominal stock prices in February.

The Roughly Coincident Indicators index was unchanged in February, holding at 75 for a fourth consecutive month. Overall, four indicators were trending higher: nonfarm payrolls, employment-to-population ratio, industrial production, and real personal income excluding transfers. One roughly coincident indicator, consumer confidence in the present situation, was trending lower, while the real manufacturing and trade sales indicator remained in a neutral trend.

AIER’s Lagging Indicators index increased to 83 in February, up from 75 in January. January and February were the first back-to-back months above neutral since November and December 2019. One lagging indicator showed improvement in February: the composite short-term interest rates indicator improved to a positive trend from a neutral trend. Overall, five indicators were in favorable trends, one indicator had an unfavorable trend, and none had a neutral trend.

Overall, ongoing disruptions to labor supply and production, rising costs and shortages of materials, and logistics and transportation bottlenecks continue to exert upward pressure on prices. While cresting numbers of new Covid cases in late January and early February had the potential to support businesses’ efforts to improve supply chains and expand production, geopolitical turmoil surrounding the Russian invasion of Ukraine has had a dramatic impact on capital and commodity markets, launching a new wave of potential disruptions to businesses. The outlook has become highly uncertain and extreme caution is warranted.

Nominal-dollar Retail Spending Rebounded in January

Retail sales and food-services spending rose 3.8 percent in January following a 2.5 percent drop in December. The strong gain suggests first quarter gross domestic product may be off to a good start. However, today’s retail sales data are not adjusted for price changes. Therefore, it’s likely that the real or price-adjusted results would be less robust. Still, total retail sales are up 13.0 percent from a year ago and remain about 11.5 percent above the pre-pandemic trend.

Core retail sales, which exclude motor vehicle dealers and gasoline retailers, also jumped 3.8 percent for the month, following a 3.2 percent fall in December, leaving that measure with a 11.4 percent gain from a year ago. Core retail sales are 9.8 percent above the pre-pandemic trend.

Most categories were up in January with eight posting increases while five showed declines. The gains were led by a 14.5 percent surge for nonstore retailers following an 11.4 percent plunge in December. Furniture and home furnishings store sales posted a 7.2 percent gain for the month followed by motor vehicles and parts dealers with a 5.7 percent gain, building material and garden equipment and supplies dealers with a 4.1 percent rise, and general merchandise stores with a 3.6 percent advance.

Sporting goods, hobby, and bookstore sales led the decliners, down 3.0 percent, followed by gasoline, down 1.3 percent, food services and drinking sales, off 0.9 percent, and health and personal care store sales, down 0.7 percent.

Real Retail Sales Remain in a Downtrend

While nominal retail sales continue to grow, the real retail sales indicator in the AIER Leading Indicators Index remains in a down trend. The Rapid acceleration in consumer prices has accounted for most if not all of the gain in nominal retail sales, resulting in a downward trend in real terms. November 2021 was the last month the real retail sales indicator was in a positive trend, with December dropping to a neutral trend and January and February both coming in with downward trends.

Overall, total and core nominal retail sales posted robust rebounds in January following steep drops in December, keeping them well above pre-pandemic trends. The strong results in January suggest that first quarter nominal gross domestic product may have gotten off to a good start. However, after adjusting for price changes, real or price-adjusted results are much weaker.

February Unit Auto Sales Slowed as Assemblies, Inventories, and Prices Stabilize in January

Sales of light vehicles totaled 14.1 million at an annual rate in February, down from a 15.0 million pace in January. The February result was a 6.4 percent fall from the prior month and was the ninth consecutive month below the 16 to 18 million range, averaging just 13.7 million. Weak auto sales are largely a result of component shortages that have limited production, resulting in plunging inventory and surging prices.

Breaking down sales by origin of assembly, sales of domestic vehicles decreased to 11.2 million units versus 12.0 million in January, a drop of 7.6 percent, while imports fell to 3.21 million versus 3.28 million in January, a decline of 2.1 percent. Domestic sales had generally been in the 13 million to 14 million range in the period before the pandemic, averaging 13.3 million for the six years through December 2019. The domestic share came in at 77.2 percent in February versus 78.2 in January.

Domestic assemblies decreased slightly in January, coming in at 9.35 million at a seasonally adjusted annual rate. That is down from 9.47 million in December but still well below the 11.2 million pace for the six years through December 2019.

Component shortages, especially of computer chips, continue to restrain production for most manufacturers, creating a scarcity for many models, leading to lower inventory and higher prices. Ward’s estimate of unit auto inventory came in at 106,700 in January, near the all-time low. Inventory may be stabilizing as the average over the last five months was 110,060 and has not dropped below 100,000. The Bureau of Economic Analysis estimates the inventory-to-sales ratio fell to 0.171 in January, a new record low, just slightly below the previous record low of 0.188 in November 2021.

The plunging inventory levels have pushed prices sharply higher over the last two years. However, prices may be stabilizing with the average consumer expenditure for a car coming in at $32,926 in January, down 1.1 percent from December. The average consumer expenditure on a light truck fell to $48,312 from $48,332 in December. The January levels represent 12-month gains of 17.7 percent and 13.7 percent, respectively.

As a share of disposable personal income per capita, average consumer expenditures on a car came in at 59.9 percent versus 60.7 in December but just 41.6 percent in March 2021 while the average consumer expenditure on a light truck as a share of disposable personal income per capita was 87.9 percent versus 88.1 percent in December and 64.5 percent as recently as March 2021. Both measures are still below their all-time highs.

Consumer Sentiment Fell Sharply in Early February

The preliminary February results from the University of Michigan Surveys of Consumers show overall consumer sentiment fell sharply in early February, hitting the lowest level since October 2011. The composite consumer sentiment decreased to 61.7 in early February, down from 67.2 in January, a drop of 8.2 percent. The index is now 19.7 percent below the year ago level and 36.5 percent below the 2018 – 2019 average.

The current-economic-conditions index fell to 68.5 from 72.0 in January. That is a 4.9 percent decrease and leaves the index with a 20.5 percent decrease from February 2021 and a 39.1 percent decline from the 2018 – 2019 average.

The second sub-index — that of consumer expectations, one of the AIER leading indicators — sank 6.7 points or 10.5 percent for the month, dropping to 57.4. The index is off 18.8 percent from a year ago and 34.2 percent from its 2018 – 2019 average.

All three indexes are now below the lows seen in four of the last six recessions.

According to the report, “The recent declines have been driven by weakening personal financial prospects, largely due to rising inflation, less confidence in the government’s economic policies, and the least favorable long-term economic outlook in a decade.” The report goes on to add, “Importantly, the entire February decline was among households with incomes of $100,000 or more; their Sentiment Index fell by 16.1% from last month, and 27.5% from last year.”

The one-year inflation expectations rose to 5.0 percent in early February, the highest level since hitting 5.1 percent in July 2008. The one-year expectations has spiked above 3.5 percent several times since 2005 only to fall back. The five-year inflation expectations remained unchanged at 3.1 percent in early February. That result remains well within the 25-year range of 2.2 percent to 3.5 percent.

According to the report, “The impact of higher inflation on personal finances was spontaneously cited by one-third of all consumers, with nearly half of all consumers expecting declines in their inflation adjusted incomes during the year ahead. In addition, fewer households cited rising net household wealth since the pandemic low in May 2020, largely due to the falling likelihood of stock price increases in 2022.”

The report adds, “The recent declines have meant that the Sentiment Index now signals the onset of a sustained downturn in consumer spending. The depth of the slump, however, is subject to several caveats that have not been present in prior downturns: the impact of unspent stimulus funds, the partisan distortion of expectations, and the pandemic’s disruption of spending and work patterns.”

Manufacturing-Sector Survey Showed Strong Results in February

The Institute for Supply Management’s Manufacturing Purchasing Managers’ Index rose to 58.6 in February, up 1.0 point from 57.6 percent in January. February is the 21st consecutive reading above the neutral 50 threshold. The survey results indicate that the manufacturing sector continues to expand despite ongoing labor and material constraints. The report suggests demand remained strong and despite complications from Covid, production improved. The report also suggests labor shortages from quits and retirements remain a significant headwind. Overall, survey respondents remain optimistic.

The new orders index rose 3.8 points to 61.7 percent in February. It has been above 50 for 21 consecutive months, and it moved back above 60 after a one-month dip below 60 in January; the index is now at the highest level since September 2021. The new export orders index, a separate measure from new orders, rose to 57.1 versus 53.7 in January. The new export orders index has been above 50 for 20 consecutive months.

The Backlog-of-Orders Index posted a strong gain in February, coming in at 65.0 versus 56.4 in January, an 8.6-point jump, to the highest level since August 2021. This measure has pulled back from the record-high 70.6 result in May 2021 but has been above 50 for 20 consecutive months. The index suggests manufacturers’ backlogs continue to rise and that the pace accelerated in February.

The Production Index registered a 58.5 percent result in February, a rise of 0.7 points from January. The index has been above 50 for 21 months and while the level is below the results of late 2020 and early 2021, the index remains at a favorable level by longer-term historical comparison.

The Employment Index pulled back in February but remained at or above neutral for the fifteenth consecutive month, coming in at 52.9 percent. Despite the slower pace of expansion in February, the run of results at or above neutral is an indication that some of the labor issues plaguing production may start to ease in coming months.

Customer inventories in February are still considered too low, with the index coming in at 31.8, off 1.2 points from January (index results below 50 indicate customers’ inventories are too low). The index has been below 50 for 65 consecutive months. Insufficient inventory is a positive sign for future production.

The index for prices for input materials fell slightly in February, off 0.5 points to 75.6 percent versus 76.1 percent in January. The index is down from a recent peak of 92.1 in June 2021 but still at a high level by historical comparison. Meanwhile, the supplier deliveries index registered a 66.1 result in February, up 1.5 points from the January result. The rise suggests deliveries slowed again in February and that the pace accelerated somewhat. While both of these indexes remain elevated by historical comparisons, they are down significantly from the 2021 peaks.

Overall, demand for the manufacturing sector remains robust but labor difficulties, materials shortages, and logistical problems continue to hamper the ability to meet that demand. While there has been some modest progress, the period of normalization has been extended by recurring waves of Covid, labor turnover, and worker retirement. The delayed return to normalcy is sustaining upward pressure on prices. Furthermore, geopolitical turmoil as a result of the Russian invasion of Ukraine has had a dramatic impact on capital and commodity markets, launching a new wave of potential disruptions to the global economy and businesses.

Services-Sector Growth Slowed by Labor, Materials, and Logistical Constraints

The Institute for Supply Management’s composite services index fell to 56.5 percent in February, losing 3.4 points from 59.9 percent in the prior month. The index remains above neutral and suggests the 21st consecutive month of expansion for the services sector and the broader economy but is now at its lowest level since February 2021. The declines over the last three months suggest that growth has likely slowed with respondents to the survey blaming labor shortages and turnover, materials shortages, logistical issues, and price pressures.

Among the key components of the services index, the business activity index fell 4.8 points to 55.1. That is the 21st month above 50 but also the lowest reading since a 40.9 result in May 2020 in the aftermath of government shutdowns that caused the worst recession in American history.

The services new-orders index fell to 56.1 percent from 61.7 percent in January, a drop of 5.6 percentage points. The new orders index has been above 50 percent for 21 months but is now at the lowest level since February 2021. For the latest month, 11 industries reported expansion in new orders while three reported drops.

The nonmanufacturing new-export-orders index, a separate index that measures only orders for export, rebounded in February, coming in at 53.0 versus 45.9 percent in January. Seven industries reported growth in export orders against two reporting declines.

Backlogs of orders in the services sector likely grew again in February as the index increased to 64.2 percent from 57.4 percent. February was the 14th month in a row with rising backlogs. Thirteen industries reported higher backlogs in February while three reported a decrease.

The services employment index dropped below the neutral 50 percent level, coming in at 48.5 percent in February, down from 52.3 percent in January and a recent high of 57.0 percent in November 2021. Seven industries reported growth in employment while eight reported a reduction.

Supplier deliveries, a measure of delivery times for suppliers to nonmanufacturers, came in at 66.2 percent, up from 65.7 percent in the prior month. It suggests suppliers are falling further behind in delivering supplies to services business and the slippage accelerated slightly from the prior month. Sixteen industries reported slower deliveries in February while none reported faster deliveries.

The nonmanufacturing prices paid index rose to 83.1 percent, up from 82.3 percent in January, and just below the all-time high in December 2021. Eighteen industries reported paying higher prices for inputs in February while none reported lower prices. The February report from the Institute of Supply Management suggests that the services sector and the broader economy expanded for the 21st consecutive month in February. Respondents to the survey continue to highlight strong demand but also continued price pressures, materials shortages, logistics, and transportation issues, and challenges hiring and retaining workers. As the latest wave of Covid fades, some improvement in production is expected, but the overall shortage of labor is likely to be a lingering problem.