{kind=link}

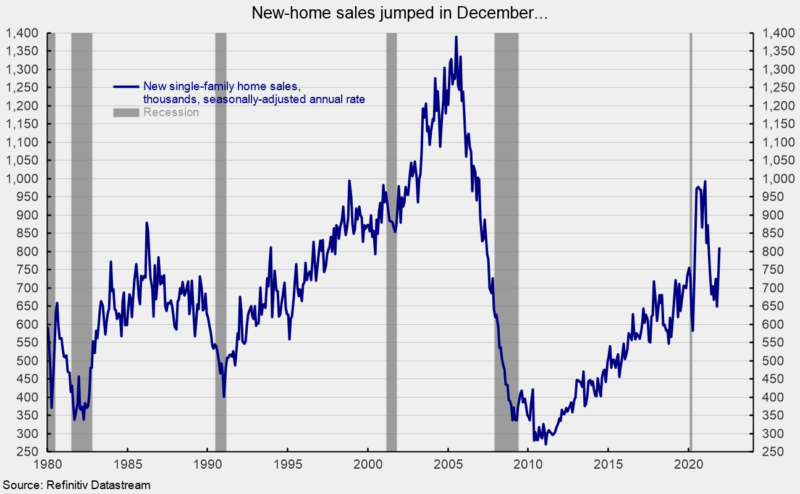

Sales of new single-family homes posted a gain in December, jumping 11.9 percent to 811,000 at a seasonally-adjusted annual rate from a 725,000 pace in November. Despite the gain, sales are down 14.0 percent from the year-ago level (see top of first chart). New home sales surged in the second half of 2020 but then slowed sharply in the first three quarters of 2021, hitting a low of 649,000 in October. Since October, sales have increased for two consecutive months (see top of first chart).

Sales of new single-family homes were up in three of the four regions of the country in December. Sales in the South, the largest by volume, rose 14.9 percent while sales in the West gained 0.4 percent, and sales in the Midwest increased 56.4 percent while sales in the Northeast were off 15.6 percent for the month. From a year ago, sales were up 2.1 percent in the West but are off 34.1 percent in the Northeast, down 23.2 percent in the Midwest and off 17.5 percent in the South.

The median sales price of a new single-family home was $377,700 (see top of second chart), down sharply from $416,100 in November (not seasonally adjusted). The gain from a year ago is just 3.4 percent versus an 18.6 percent 12-month gain in November (see bottom of second chart). On a 12-month average basis, the median single-family home price is still at a record high (see top of second chart).

Despite the jump in sales, the total inventory of new single-family homes for sale rose 1.5 percent to 403,000 in December, putting the months’ supply (inventory times 12 divided by the annual selling rate) at 6.0, down 9.1 percent from November but 57.9 percent above the year-ago level (see third chart). The months’ supply is at a relatively high level by historical comparison and is substantially higher than the months’ supply of existing single-family homes for sale (see third chart). The relatively high months’ supply may be one reason for the plunge in median home price. The median time on the market for a new home remained very low in December, coming in at 2.8 months versus 2.9 in November.

Record-high prices and higher mortgage rates (see fourth chart) are headwinds forcing some buyers out of the market. However, the rise of more flexible working arrangements (i.e. remote work) may provide some continued support for less dense housing.

Furthermore, while somewhat elevated months’ supply and rising mortgage rates impact supply and demand balance, elevated material costs (see fifth chart) may be squeezing profit margins for homebuilders.